MARKET UPDATE

UK & International

1st quarter 2026 Report

Market Summary update

Q1 2026 Report

This Q1 2026 report from Kukla Beverage Logistics provides an operational overview of road, sea, air and rail freight and the key factors affecting beverage supply chains across the UK, Europe and global trade lanes.

OVERVIEW

Q1 2026 should have been a relatively stable market, with capacity returning across most modes following the Q4 peak.

In practice, reliability remained the key issue across UK import lanes, including Italy, Spain, France, South Africa, Australia, New Zealand and the United States, rather than space availability.

Whilst recurring disruption across UK ports, Benelux hubs and Iberian services meant routing and delivery planning had to be adjusted continually.

Market signals

- Ongoing disruption across ports, weather-affected corridors and infrastructure constraints defined operating conditions in Q1, with ongoing pressure on reliability and equipment availability.

- Fuel volatility increased towards the latter part of the quarter, linked to geopolitical developments in the Middle East.

- Security risk remained present across the quarter. While overall levels were stable, exposure increased in areas where extended dwell times and delayed collections occurred.

Road Freight

Cost pressure with limited recovery time

Road freight continues to underpin beverage logistics across Europe, particularly on key lanes such as Italy–UK and Spain–UK, as well as onward distribution into bonded and retail networks.

- Road freight remains central to European beverage logistics, supporting key Italy–UK and Spain–UK lanes as well as bonded and retail distribution.

- Network disruption reduced vehicle productivity and placed sustained pressure on delivery schedules.

- Across Europe, congestion and weather disruption have extended transit times and reduced flexibility on core corridors.

Rail Freight

European rail freight remained a useful option across Q1, particularly for structured UK–Europe beverage flows. However, performance was shaped less by demand and more by infrastructure pressure, congestion and disruption on key corridors.

Rail congestion in Italy, backlog at Barcelona and wider weather-related disruption across Europe all reduced flexibility during the quarter. The main message is clear: rail remained viable, but reliability depended on planning, routing discipline and network stability.

aiR Freight

Targeted capacity, operational adjustment. Air freight remained a supporting mode in Q1, with stable capacity but ongoing routing constraints and variable transit performance.

Sea Freight

Ocean freight conditions in Q1 reflected adequate capacity across key beverage import trades.

However, stable capacity did not translate into stable execution. Operational factors continued to have a greater influence on performance than headline market conditions.

UK imports continued to be affected by congestion and operational disruption at key ports. Delays in container discharge, collection and terminal handling reduced flow through the network and impacted onward transport planning.

Rotterdam, Antwerp, and Iberian services have also been disrupted by congestion and adverse weather.

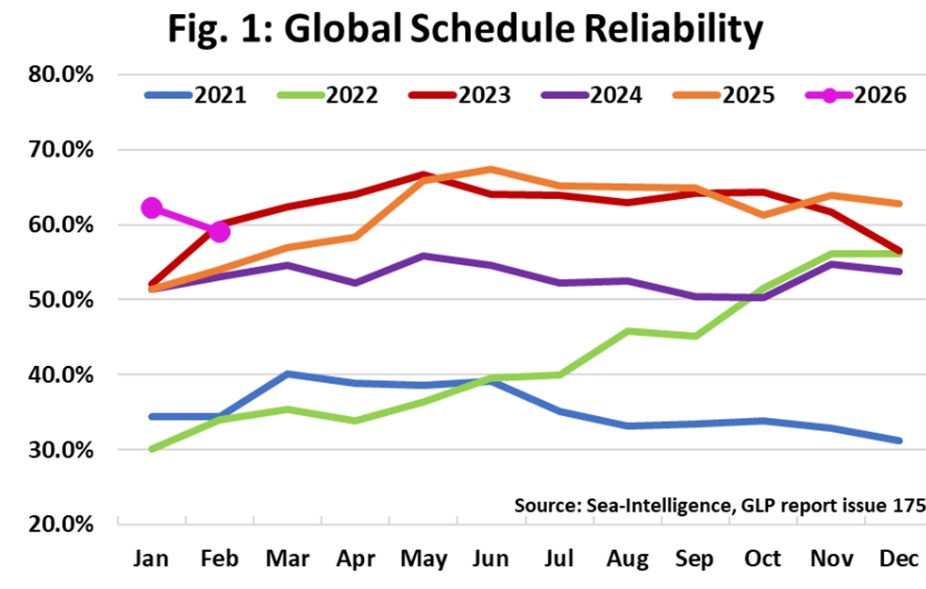

Schedule reliability has also weakened, with global performance falling to 59% in February. This reflects continued instability across carrier networks, with delays and service changes affecting predictability across multiple trades.

Multimodal and short sea services remain important across UK–Europe flows, but performance is closely tied to infrastructure stability. Rail congestion and terminal backlogs have continued to affect key corridors, limiting flexibility where timing is critical.

At the same time, fuel volatility and surcharge fluctuations are adding further uncertainty. The overall position remains unchanged: while rates appear favourable, reliability and total landed cost continue to be driven by operational conditions rather than pricing alone.

Freight SECURITY

Extended dwell times and network disruption have increased exposure in Q1. Controlled planning and secure operations remain essential to protect cargoes.

ROAD FREIGHT MARKET OVERVIEW

European road freight: operational pressure and reduced recovery capacity

- Road freight remained central to beverage logistics across Europe, particularly on Italy–UK, Spain–UK and bonded distribution flows.

- Network resilience was reduced during Q1 by winter weather, local restrictions and limited recovery capacity across key European corridors.

- Port-related disruption in the UK affected container collections and onward haulage on multimodal flows, placing pressure on vehicle productivity and delivery schedules.

- Accurate booking, realistic lead times and strong load preparation became increasingly important as recovery options narrowed.

Road freight remained under operational pressure in Q1, with winter weather, local restrictions and limited recovery capacity reducing flexibility across key European corridors. While trailer-based road operations were not directly affected by congestion at major LoLo container hubs such as Rotterdam and Antwerp, wider disruption across ports, terminals and connected networks added pressure to multimodal planning, equipment positioning and schedule recovery.

Key pressure points remained consistent across Europe:

In the UK, disruptions at key ports affected container collection and onward haulage for multimodal flows, reducing vehicle productivity and putting pressure on delivery schedules.

January saw adververse winter conditions across the Netherlands, France, Germany and Northern Italy. Further weather warnings and local restrictions continued to affect planning. Routes remained open, but with limited resilience and recovery.

Congestion at Rotterdam and Antwerp remained relevant primarily to container and multimodal flows, with indirect effects on equipment availability, recovery capacity and wider Benelux network conditions. These factors did not directly affect trailer-based road movements via RoRo ports, but contributed to overall pressure on planning and execution.

In Italy, local restrictions and scheduled driving bans added further constraints. In Spain, weather disruption in the Bay of Biscay and backlog at the Barcelona terminal affected connected multimodal planning and narrowed delivery windows.

The operational effect included delayed collections, restricted Vehicle Booking System (VBS) access and limited scope to recover schedules without additional cost.

SEA FREIGHT GLOBAL MARKET OVERVIEW

sea freight RELIABILITY

Sea Freight: stable capacity, but inconsistent execution

Ocean freight conditions in Q1 reflected adequate capacity across key beverage import trades, including South Africa–UK, Australia/New Zealand–UK and parts of the US–UK corridor. However, this did not translate into consistent operational performance.

Service reliability remained the primary constraint:

- UK imports affected by congestion at key UK ports

- Rotterdam and Antwerp congestion continued to extend transit times

- Iberian services disrupted by weather in the Bay of Biscay, delaying sailings

- South Africa, Australia/New Zealand and U.S. lanes affected by delays, omissions and reduced booking reliability

Global schedule reliability fell to 59% in February, reflecting ongoing instability in carrier performance and increasing average delays.

Short sea and multimodal services remained important for UK–Europe flows, but performance was closely linked to wider infrastructure. Rail congestion in Italy, backlog in Barcelona and the Rheintalbahn closure reduced capacity and flexibility across connected inland networks.

Disruption remained a constant operating condition. Port congestion, weather delays and infrastructure constraints across Europe continued to affect execution across all major beverage lanes.

Fuel volatility added further pressure. Emergency surcharges fluctuated, and rising diesel costs across Europe increased overall transport spend. Available capacity did not translate into lower landed cost.

Operational impact for beverage logistics:

- Reliability remained inconsistent despite lower rates

- Planning required longer lead times and flexible routing

- Documentation accuracy remained critical for bonded and mixed loads

- Load quality and pallet stability became more important as handling and delays increased

- Reduced dwell time and secure parking remained essential to mitigate freight crime risk

The key point remains unchanged: execution, reliability and total landed cost continue to be driven by operational disruption rather than base freight rates.

Ongoing disruption to global routing, including longer diversion patterns on certain trades, is beginning to influence transit consistency and equipment availability.

RAIL FREIGHT MARKET OVERVIEW

European rail freight: relevant, but increasingly infrastructure-led

European rail freight remained an important part of beverage logistics in Q1 2026, particularly where multimodal solutions were used to support UK–Europe flows.

In practice, however, performance across the quarter was increasingly shaped by infrastructure and network stability rather than by available demand. Congestion continued across the Italian rail network, which remained a recurring issue throughout January, February and March.

On Iberian flows, the backlog at the Barcelona terminal and disruption following earlier service issues reduced operational capacity.

A further occurrence in Q1 was the planned closure of the Rheintalbahn route between Offenburg and Basel, which highlighted the extent to which European rail remains reliant on a relatively small number of key freight arteries. Alternative routing allowed services to continue, with operational limitations on train length and weight, which, in turn, reduced overall capacity.

The weather was also a continuing factor. Winter disruption across parts of Northern and Central Europe affected broader transport operations during the quarter, with rail performance influenced by wider pressures from across connected road and terminal infrastructure.

Freight crime

Managing risk through controlled operations

Extended dwell times linked to congestion, delayed collections, and network disruption, resulting in increased exposure in certain areas of the UK. This was in part due to vehicles being held longer than planned or requiring routing adjustments.

From an operational perspective, this reinforces the importance of controlled planning and execution. Route selection, secure parking, seal management and minimising dwell time remain essential components of a consistent operational approach.

At Kukla, these measures are embedded into day-to-day operations, ensuring that risk is actively managed alongside service performance.

AIR FREIGHT MARKET OVERVIEW

Air Freight Key Data Highlights:

- Capacity remained available, but disruption across sea and road increased reliance on air for time-critical shipments.

- Global air cargo volumes projected to grow by 2.4% in 2026.

- Performance remained variable, with transit times typically 5–7 days.

Air freight bookings in Q1 reflected both planned movements and critical shipments, with demand rebounding following the slowdown in late 2025.

Capacity across key UK gateways remained stable, supported by passenger belly hold space. However, demand was influenced by global disruptions, resulting in some movements shifting to air, where timing risk increased.

Performance remained dependent on flight availability, airport handling and customs clearance. Transit times were typically 5–7 days, but remained variable where capacity was constrained or documentation was delayed.

Airspace restrictions across parts of the Middle East are reducing routing options on some corridors, requiring aircraft repositioning and re-routing, leading to extended transit times.

BEVERAGE LOGISTICS

MANAGING OPERATIONAL COMPLEXITY THROUGH EXPERTISE AND CONTROL

The primary operational requirements across beverage logistics remained consistent in Q1, with performance increasingly dependent on accuracy, preparation and timing discipline.

- Documentation accuracy remained critical, particularly for mixed loads and bonded movements. Precision helps avoid unnecessary delays and ensures compliance throughout the supply chain.

- Load quality continues to play an important role. Consistent palletisation, stable stacking and appropriate wrapping are essential as transit times extend and handling increases.

- Timing discipline has become increasingly important. With limited recovery options across the network, early booking and shipment readiness were key to maintaining schedule integrity.

Recommendations for beverage shippers

In current market conditions, performance is driven by planning and execution.

Bookings should be made with sufficient lead time, particularly on congested or weather-affected lanes. Flexibility in routing, especially across UK ports and European hubs, remains important.

Documentation should be completed accurately and in full prior to movement. Errors continue to be a primary cause of avoidable delays.

Pallet preparation should follow consistent standards, ensuring stability, clear labelling, and minimal risk of mixed products.

Outlook for Quarter 2 2026

Q2 outlook: external pressure

The key external factor entering Q2 is the ongoing situation in the Middle East and its impact on energy markets and global shipping patterns.

Fuel volatility is expected to remain a primary influence on transport costs, with diesel and bunker prices reacting quickly to geopolitical developments. This will continue to affect surcharges across ocean, air and road freight.

At the same time, disruption to key shipping routes is likely to influence equipment positioning, schedule reliability and overall network balance. Changes in vessel routing and capacity allocation may continue to impact transit consistency across long-haul trades.

From a European perspective, these external pressures will combine with existing infrastructure constraints. This means that reliability and total landed cost will remain closely linked to operational conditions rather than solely to base rates.

Road freight will remain influenced by cost pressure and network constraints. Rail will continue to offer alternatives but remain dependent on infrastructure availability.

Airspace restrictions and corridor disruptions are also affecting routing options, requiring aircraft repositioning and contributing to ongoing variability in transit times.

Conclusion: managing this complexity through experience and expertise

Current market conditions require a consistent and operationally focused approach.

At Kukla Beverage Logistics, this is managed through a combination of carrier diversification, detailed market knowledge and close coordination across all stages of the supply chain.

Our balanced portfolio allows flexibility across routes and services, reducing dependency on any single carrier. This approach enables us to respond quickly and efficiently to changing conditions whilst maintaining continuity across beverage supply chains.